With so much uncertainty surrounding the economy due to the Coronavirus (COVID-19), some are concerned that we could face another housing crash like we faced in 2008.

This concern is understandable. Ali Wolf, Director of Economic Research at the real estate consulting firm Meyers Research, has addressed this point in a recent interview:

“With people having PTSD from the last time, they’re still afraid of buying at the wrong time.”

Compass San Diego Manager, Steve Salinas, talks about the five Indicators that will ease concerns relating to the future of the real estate market.

"I certainly cannot predict the future, but if I look at the underlying principles there are many reasons, indicating this real estate market is nothing like 2008. Here are five points that highlight the differences.

1. Mortgage standards are nothing like they were back then

During the housing bubble, it was easy to get a mortgage. Lenders used to joke about the 'fog test'. If they held a mirror in front of you and if you fogged the mirror, you qualified. As anyone who has gone through the process recently knows, it is tough to qualify. The Mortgage Bankers’ Association released a Mortgage Credit Availability Index which is “a summary measure which indicates the availability of mortgage credit at a point in time.” The higher the index, the easier it is to get a mortgage. During the housing bubble, the index skyrocketed. Currently, the index shows how getting a mortgage is exponentially more stringent.

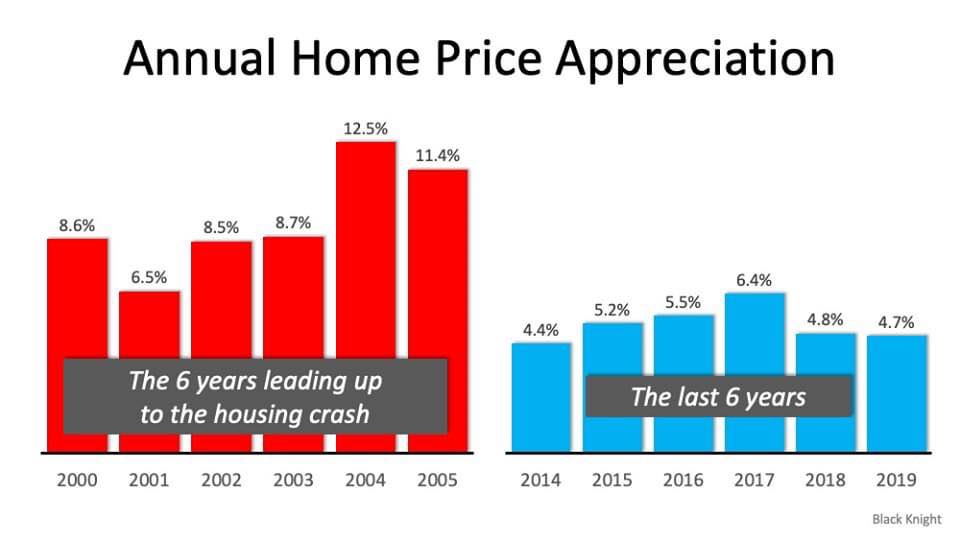

2. Prices have not been soaring out of control

Price appreciation has been quite strong recently, but it is nowhere near the rise in prices that preceded the crash. There is a dramatic difference between the two periods of time. Normal appreciation is 3.6%, so while current appreciation is higher than the historic norm, it’s certainly not accelerating beyond control as it did in the early 2000s.

3. We don’t have a surplus of homes on the market. We have a shortage

The supply of inventory needed to sustain a normal real estate market is approximately 6-7 months. Anything more than that is an overabundance and will cause prices to depreciate. Anything less than that is a shortage and will lead to continued appreciation. In 2007 there were too many homes for sale and that caused prices to fall. Today, there’s a shortage of inventory.

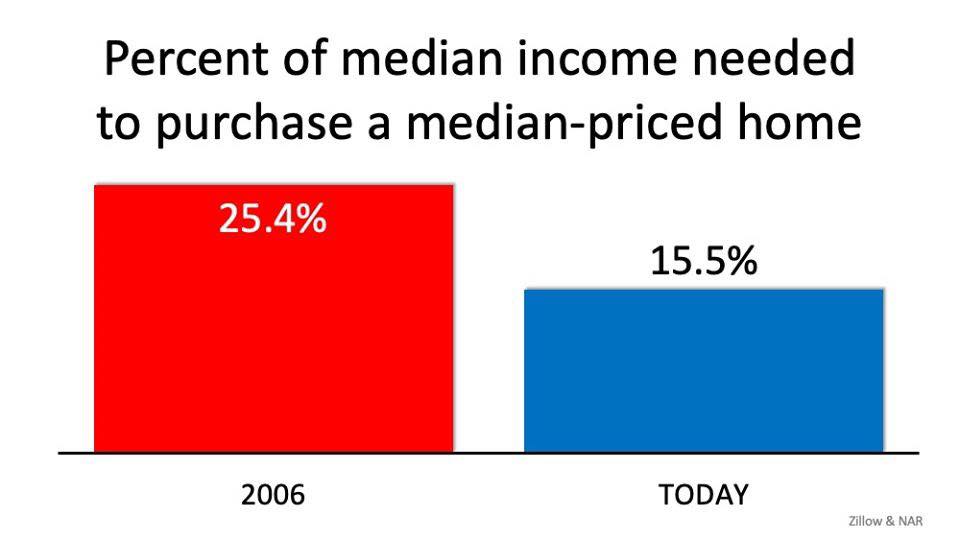

4. The wage to mortgage ratio has improved

The affordability formula has three components: the price of the home, the wages earned by the purchaser, and the mortgage rate available at the time. Fourteen years ago, prices were high, wages were low, and mortgage rates were over 6%. Today, prices are still high. Wages, however, have increased and the mortgage rate is about 3.5%. That means the average family pays less of their monthly income toward their mortgage payment than they did back then.

5. People are equity rich, not tapped out.

Prior to the housing bubble, homeowners were using their homes as a personal ATM machine. We all remember everyone had a new boat and SUV parked in front of their house. It was common and socially accepted that most withdrew their equity once it built up. The housing crash was a cruel teacher for many, but most learned their lesson. Prices have risen nicely over the last few years, leading to over 50% of homes in the country having greater than 50% equity. Current homeowners have withdrawn over $500 billion dollars less than previous homeowners did during the crash. This places most homeowners in a better position to weather a storm. In addition, the motivation to just walk away is less if you have substantial equity still in your home.

Think positively when we look at the core principles above we are positioned exponentially better than we were in 2008."